For years, that bulky billfold felt like a badge of honor, a leather-bound record of our lives. However, in today’s world, it has become less of a personal archive and more of a personal liability. A lost or stolen wallet is a goldmine for identity thieves, and the stakes are higher than ever.

Just how high? In 2021 alone, the Bureau of Justice Statistics reported that approximately 23.9 million people in the U.S. became victims of identity theft, resulting in a total financial loss of $16.4 billion. And this isn’t just a problem for the younger generation. In fact, it’s the opposite. People ages 50 to 64 are more likely to be victims of identity theft than any other age group.

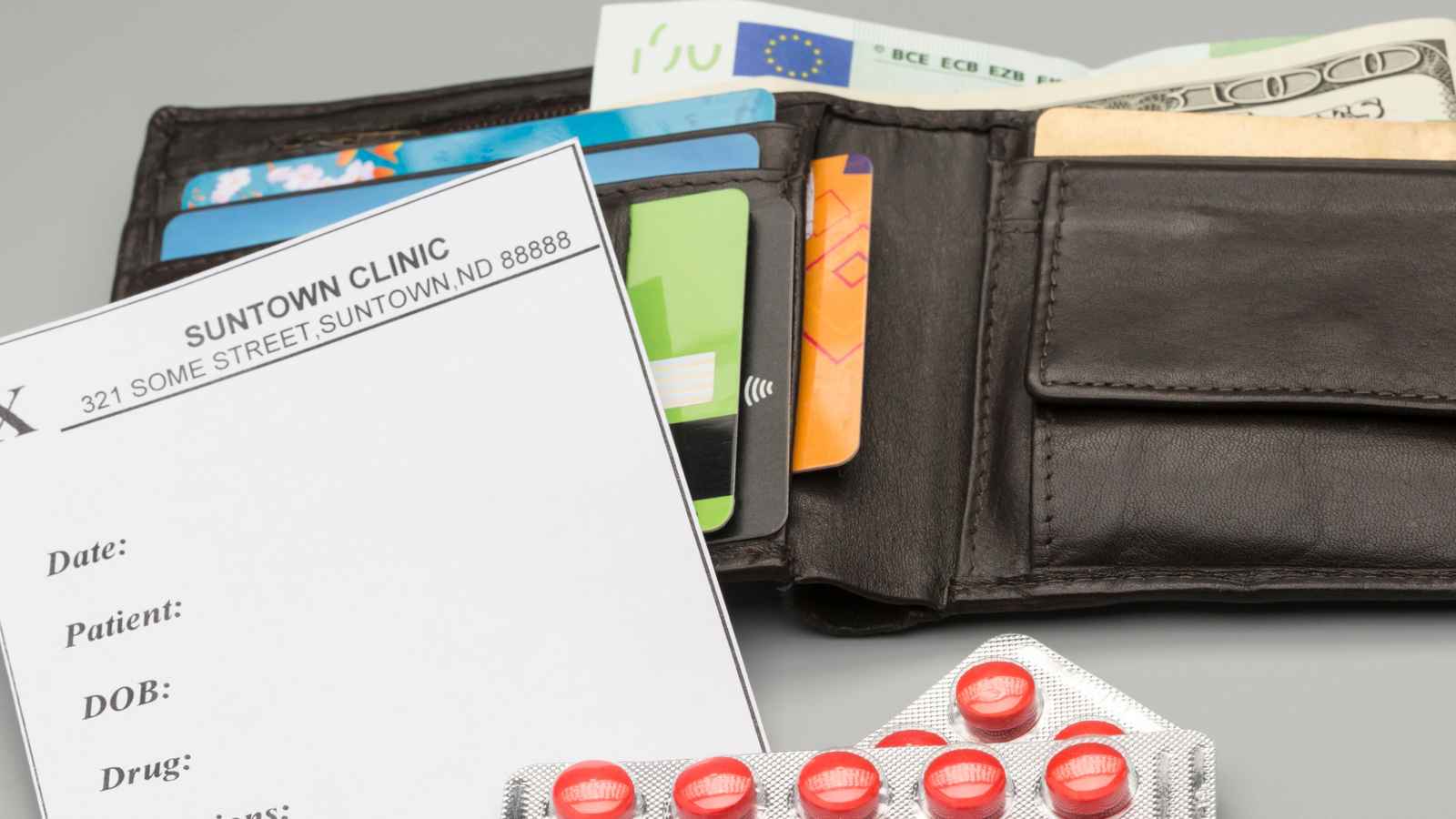

Anything convenient for you would be convenient for a thief… The most harmful things in your wallet are things that have long-term costs.

So, let’s talk about lightening the load. Slimming down your wallet isn’t just about decluttering—it’s one of the simplest, most powerful moves you can make to protect your finances, your identity, and your peace of mind. Ready to do a wallet detox?

A Spare House Key

Carrying a spare key next to your driver’s license is like handing a burglar a map and a key to your front door. It seems so convenient, right? But it’s a terrible idea. A lost wallet that contains both your home address (thanks, driver’s license!) and a key to access your home is a “treasure map for thieves.”

While you’re on the phone frantically canceling your credit cards, a thief could already be inside your home. Even if you avoid a break-in, the cost of hiring a locksmith to change the locks for your own peace of mind will likely run you more than $100.

The Modern Solution: The safest place for a spare key is with a trusted neighbor, friend, or family member. If you’re looking for a tech-forward solution, consider installing a smart digital lock. You can open it with a code, your fingerprint, or your phone, eliminating the need for a physical key.

Your Entire Checkbook (or Even One Blank Check)

Carrying a blank check is like signing a permission slip for a thief to drain your bank account. A single blank check is a treasure trove of sensitive data: your name, address, bank name, routing number, and full account number. That’s everything a criminal needs to either forge your signature and cash a check or, more likely these days, set up electronic withdrawals from your account.

Worse yet, your liability is much higher than with credit card fraud. With checks, you could be liable for up to $500 if you don’t report the fraud within two days, and potentially the entire stolen amount if you wait longer than 60 days.

The Modern Solution: Leave the checkbook at home. It’s becoming increasingly rare to need a check unexpectedly. If you know you need to write one for a specific errand, bring that single check with you. For everything else, a debit card or a peer-to-peer (P2P) payment app like Zelle or Venmo is a faster, easier, and more secure option.

Your Passport or Passport Card

Unless you’re boarding an international flight today, your passport’s safest place is locked up at home. This is a non-negotiable. The U.S. State Department itself refers to the American passport as “the most valuable identity document in the world.” To criminals, it’s pure gold.

A stolen passport can be sold on the dark web for a high price or used by a criminal to travel in your name, open fraudulent bank accounts, or even try to get a copy of your Social Security card.

Losing your driver’s license is a headache. Losing your passport is a severe crisis that can require a significant amount of time and effort to resolve.

The Modern Solution: Your state-issued driver’s license is all you need for daily identification. When traveling abroad, financial expert Clark Howard offers some valuable advice: take a picture of the key pages of your passport and store it on your phone. Then, lock the physical passport in your hotel safe. That photo makes getting an emergency replacement much, much easier if the worst happens.

A Password Cheat Sheet

A password list in your wallet completely defeats the purpose of having passwords.

You’d be surprised how many people do this. A 2023 Pew Research Center survey found that 41% of U.S. adults admit to writing their passwords down on paper. It’s the digital equivalent of leaving your key under the doormat.

If your wallet gets stolen, the thief doesn’t just have your credit cards; they have the keys to your entire digital life—your email, bank accounts, social media, and everything.

The Modern Solution: It’s Time to Embrace a Password Manager. Apps like LastPass, 1Password, or the password managers built right into Apple and Android devices are lifesavers. They create and remember incredibly complex, unique passwords for every single one of your accounts. All you have to do is remember one strong master password.

For ironclad security, go one step further and enable two-factor authentication (MFA) on any account that offers it. It’s that little code texted to your phone, and it’s one of the best defenses you have.

A Wallet Full of Cash

In our increasingly digital world, carrying a fat wad of cash makes you a target, not a big shot. The age of the cash-stuffed wallet is fading fast. A Pew Research survey found that 41% of Americans now say they make no cash purchases in a typical week.

Why the shift? First, flashing a lot of cash can make you a target for robbery. Second, and more importantly, if your wallet is lost or stolen, you can cancel your credit cards and limit your losses. But that cash? It’s just gone. Forever.

The Modern Solution: Go “cash-lite.” It’s still a good idea to have a little emergency cash—say, a $20 or $50 bill—tucked away for those rare situations where cards aren’t an option.

The data shows cash hasn’t disappeared, but its role has changed. It’s now primarily used for small-value purchases (under $25) and as a backup payment method, especially among adults 55 and older. So, the smart move isn’t to abandon cash completely but to carry just enough for those specific moments, and rely on the security of cards and digital payments for everything else.

Your Medicare Card (Unless You’re Heading to the Doctor)

Treat your Medicare card like sensitive legal paperwork—only carry it when you absolutely need it.

Although the government wisely stopped printing Social Security numbers on new Medicare cards, your unique Medicare number remains a valuable piece of data for scammers. In the wrong hands, it can be used to file fraudulent claims for medical services and equipment, leaving you to sort out the mess.

This type of medical identity theft can be particularly nasty, as it can create errors in your health records that could potentially impact your future care.

The Modern Solution: The AARP provides clear and straightforward advice: only carry your Medicare card when you are actually on your way to a doctor’s office, pharmacy, or hospital. If you have a Medicare Advantage plan, you’ll likely only need your plan’s ID card for most services anyway. The rest of the time, keep your Medicare card stored securely at home.

Unspent Gift Cards

That pile of gift cards in your wallet is just like a stack of cash waiting to be lost or stolen.

You may be surprised to learn how much money is being lost due to forgotten plastic. A 2024 Bankrate survey found that over two in five U.S. adults are holding onto unused gift cards, totaling an estimated $27 billion nationwide. The average person has $244 worth of unspent value just lying around.

The problem is, a gift card is essentially cash. If a thief steals your wallet, they can spend that balance with no questions asked, and there’s no way to recover it. Additionally, we struggle with managing them ourselves.

The Modern Solution: Treat a new gift card like a check that needs to be deposited. The moment you receive one, take action. Many major retailers, such as Amazon and Target, allow you to load the balance directly into your account through their mobile app. For other cards, make a conscious plan to use them within the week. Don’t let them become permanent, risky residents of your wallet.

Old, Crumpled Receipts

Those old receipts are more than just clutter; they’re breadcrumbs for scammers and a potential health risk. From a security perspective, receipts can be surprisingly dangerous.

For example, a thief finds your wallet. They see a receipt from Best Buy for $150 with the last four digits of your Visa card. They can then call you, pretending to be from Visa’s fraud department, and say, “We’re calling to verify a recent charge of $150 at Best Buy.” Because they include those details, they appear legitimate, and they may trick you into disclosing more sensitive information.

But there’s another, hidden danger. Most of those shiny, thermal-printed receipts are coated with chemicals like BPA or its equally concerning cousin, BPS. Studies have shown that these hormone-disrupting chemicals can be absorbed through your skin after just 10 seconds of handling.

The Modern Solution: Go paperless. Ask for an e-receipt whenever you can. If you need to keep a paper receipt for an expense report or a potential return, use an app like Evernote or just your phone’s camera to snap a digital copy, then shred the original.

A Stack of Credit Cards

Carrying a wallet full of credit cards is like setting out a buffet for fraudsters. It may seem wise to have options, but from a security standpoint, it poses a significant risk. Think about it. If your wallet disappears, every card in it is a ticking time bomb. A thief can start racking up charges online or in different stores long before you’ve even noticed it’s gone. The more cards you carry, the more frantic phone calls you have to make to cancel everything, and the greater your exposure to widespread fraud.

The Modern Solution: Choose your favorite daily-driver card and leave the rest locked up at home. For even better security, load your cards into a digital wallet on your smartphone.

Many people over 50 are wary of mobile payments, but the reality is that they are far more secure than physical cards. When you use Apple Pay or Google Pay, the merchant never sees your actual credit or debit card number. Instead, the transaction uses a unique, one-time-use code through a process called tokenization.

This represents a significant security upgrade from a physical card’s magnetic stripe or chip, which can be easily copied or cloned. Plus, your phone is locked with your face or fingerprint—a level of protection your leather wallet can’t match.

Your Birth Certificate

Your birth certificate is a foundational document that establishes your identity. It has no business being in your daily-carry wallet.

This one should be a no-brainer, but it happens. Like your passport or Social Security card, your birth certificate is a high-value target for identity thieves. It contains key pieces of personally identifiable information that a criminal can use to build a fraudulent profile and cause you serious problems.

You seldom need to present your birth certificate for any day-to-day transaction.

Save this article

The Modern Solution: This document should be stored in a secure location at home, such as a fireproof safe or a locked file cabinet, alongside your other vital records. If you ever need it for an official reason (such as applying for a passport), please call ahead to see if a copy will suffice. If you must bring the original, make it a single-purpose trip: take it there, complete your business, and get it straight back home.

Your work ID badge

A lost work badge doesn’t just risk your own security—it can open the door to an attack on your entire company. The most apparent risk is physical. If your badge falls into the wrong hands, it could allow an unauthorized person to access your office building, posing a threat of theft or worse.

But in our digital age, the bigger threat is often social engineering. A badge with your photo, name, and company logo is a perfect tool for a scammer. They can use it to craft a compelling phishing email, pretending to be from HR or IT, and send it to you or your colleagues. One wrong click could lead to a major corporate data breach.

The Modern Solution: Treat your work ID with the same level of care you give your credit cards. Don’t leave it on your car’s dashboard, and avoid carrying it with you on weekends or days when you aren’t going into the office. If your company offers a digital version of your ID that you can store in your phone’s wallet, that’s often a more secure choice, since your phone’s lock screen protects it.

Your Social Security Card

Your Social Security card is the master key to your identity; carrying it is like handing a master key to a thief. This is the one thing every single security expert agrees on. Even the U.S. government’s website explicitly recommends leaving your card in a safe place at home. It is the “holy grail for identity thieves,” and losing it is a fast track to a world of hurt.

With those nine little digits, a fraudster can open new credit cards, take out loans in your name, or even file a phony tax return to steal your refund. They can also create what’s known as a “synthetic identity” by combining your real Social Security number with fake information—a type of fraud that is incredibly difficult to detect and unravel.

And the cleanup is a nightmare. While some simpler cases may be resolved in a month, the IRS’s own data from 2025 showed that its processing of identity theft victim cases averaged a staggering 582 days. Some victims report spending years trying to clear their name and fix their credit.

The Modern Solution: Memorize your number. It’s only nine digits. For those rare times when you need the physical card, such as for a new job or a home closing, take it with you for that specific purpose and bring it straight back home to its secure spot afterward.

Other people’s business cards

Your wallet is not a Rolodex. Turn new contacts into digital connections before the card gets lost in the clutter. We’ve all done it. You meet someone at a conference, they hand you their card, and you tuck it in your wallet with the best of intentions… only to find it three months later, crumpled and forgotten.

This isn’t a massive security threat, but it’s a classic example of physical clutter in a world that has moved on. It’s inefficient and leads to missed networking opportunities.

The Modern Solution: Digitize your contacts immediately. The moment you get a card, use your phone’s camera or an app like CamCard to scan it and save the information directly to your contacts.

Even better, the world of business cards is going digital. The market for apps like Blinq, HiHello, and Popl is experiencing explosive growth. These services enable you to create a digital card that can be shared instantly via a QR code or by tapping your phone, eliminating the need for paper.

A Pile of Loyalty Cards

You no longer need a deck of plastic cards to receive your grocery store discount.

That stack of cards for the pharmacy, the coffee shop, the grocery store, and the auto parts store is a classic source of wallet bloat. While seemingly harmless, some of these cards can contain personal information, such as your name and address, adding another small piece to the identity puzzle for a potential thief.

Mainly, though, they’re just unnecessary bulk in an era of apps.

The Modern Solution: There’s an app for that! The U.S. loyalty program market is massive, projected to reach over $27 billion by 2025, and it’s all driven by digital integration.

Nearly every major retailer, from Starbucks to CVS, has its own app that allows you to track your points and access your rewards. For all others, you can use a wallet aggregator app, such as KeyRing or Stocard. These let you scan the barcode from all your physical cards and store them in one place on your phone. When you check out, pull up the barcode on your screen for the cashier to scan. Easy.

Expired Credit or Debit Cards

An expired card is not just useless plastic; it’s a security risk that needs to be disposed of properly.

You might think an expired card is worthless, but it still has your full name and, most importantly, your account number printed right on it. While your new card has a different expiration date and CVV code, a determined fraudster might still be able to use that old information. Some experts have noted that it’s possible for merchants to “force post” a transaction to an old or closed card number in certain situations.

Why take the risk? An old card is another piece of your financial identity that you don’t want floating around.

The Modern Solution: Don’t just throw it away. Eradicate it. The most effective method is to use a cross-cut shredder specifically designed to handle plastic cards. If you don’t have one, grab a heavy-duty pair of scissors and get to work. Make sure you cut through the EMV chip, the magnetic stripe, your name, and every digit of the account number. For an extra layer of security, dispose of the pieces in different trash bags.

A Physical Photo of Your Kids

Your smartphone is the best family photo album you could ask for—let your wallet focus on security.

This is a sentimental one, and the advice here has changed over time. Your smartphone is already packed with hundreds, if not thousands, of high-quality photos of your loved ones. If someone asks to see a picture, you’re going to pull out your phone, not a “dusty, dented school photo” from your wallet.

More importantly, from a security perspective, a physical photo could potentially be used against you in a social engineering scam, like the infamous “grandparent scam,” where a criminal uses personal details to make their story more believable.

The Modern Solution: Let your wallet be a lean, secure tool for your financial life. Your phone is the perfect place for your treasured family photos. The significant risk of losing your critical financial and identity documents far outweighs the slight, unproven chance that an image might help get your wallet returned today.

Your Cryptocurrency Seed Phrase

Writing down your crypto recovery phrase and putting it in your wallet is the digital equivalent of taping your house key to your front door.

This one is for the growing number of people venturing into the world of digital assets, such as Bitcoin or Ethereum. A “seed phrase” or “recovery phrase” is a list of 12 or 24 words that acts as the master key to your entire crypto wallet.

This is catastrophic. If a thief finds that piece of paper, they can instantly and irreversibly drain your crypto accounts. There is no bank to call for help, no fraud department to reverse the charges. The funds are gone forever.

The Modern Solution: Your seed phrase should never be stored digitally on a computer or phone, and it should absolutely never be in your wallet. It must be stored offline, in a highly secure physical location—think a fireproof safe at home or a bank’s safe deposit box. Treat it with the utmost discretion and secrecy.

Key Takeaway

It’s Time for a Wallet Detox. In 2025, a bulky wallet is more than just an inconvenience—it’s a significant security risk. People over 50 are a prime target for identity thieves, making it necessary to minimize the amount of personal information you carry daily.

Embrace Digital, But Be Smart. The good news is that the shift to a digital world allows you to replace most of the physical clutter in your wallet with more secure and convenient apps on your phone. Digital wallets, password managers, and loyalty apps offer enhanced security features, such as tokenization and biometrics, that physical cards can’t match.

Think Like a Minimalist. The core principle is simple: carry only what you absolutely need for that specific day. For everything else—from your passport and Social Security card to spare keys and unspent gift cards—the safest place is locked up at home. A lighter wallet leads to a lighter mind and a much, much more secure financial life.

Disclaimer – This list is solely the author’s opinion based on research and publicly available information. It is not intended to be professional advice.

Like our content? Be sure to follow us

How Total Beginners Are Building Wealth Fast in 2025—No Experience Needed

How Total Beginners Are Building Wealth Fast in 2025

I used to think investing was something you did after you were already rich. Like, you needed $10,000 in a suit pocket and a guy named Chad at some fancy firm who knew how to “diversify your portfolio.” Meanwhile, I was just trying to figure out how to stretch $43 to payday.

But a lot has changed. And fast. In 2025, building wealth doesn’t require a finance degree—or even a lot of money. The tools are simpler. The entry points are lower. And believe it or not, total beginners are stacking wins just by starting small and staying consistent.

Click here and let’s break down how.

Don’t Swipe Until You Read This: The 7 Best Credit Cards for 2025 Ranked by Rewards

The 7 Best Credit Cards for 2025 Ranked by Rewards

There’s this moment that sticks with me—standing at a checkout line, swiping my old card like I always did, and thinking, “Wait… why am I not getting anything back for this?” I wasn’t traveling on points. I wasn’t getting cash back. I was spending. Sound familiar?

Look, the truth is, credit cards can work for you—if you choose the right one. And in 2025, you’ve got some advantageous options that can actually boost your bank account. From travel lovers to grocery haulers, there’s something for everyone.

Let’s break down the best credit cards out there this year—the ones that actually give back.